Few alive today in the West have experienced destitution. Yes, baby boomers raised on working class streets knew the haunted look of mothers with too much week and too little money. I recall – I’d be seven or eight 1 – the despair and humiliation on the face of one whose kids I played with, as she fled a local grocer’s under the silent gaze of a line of customers after failing to get milk and other basics on tick.

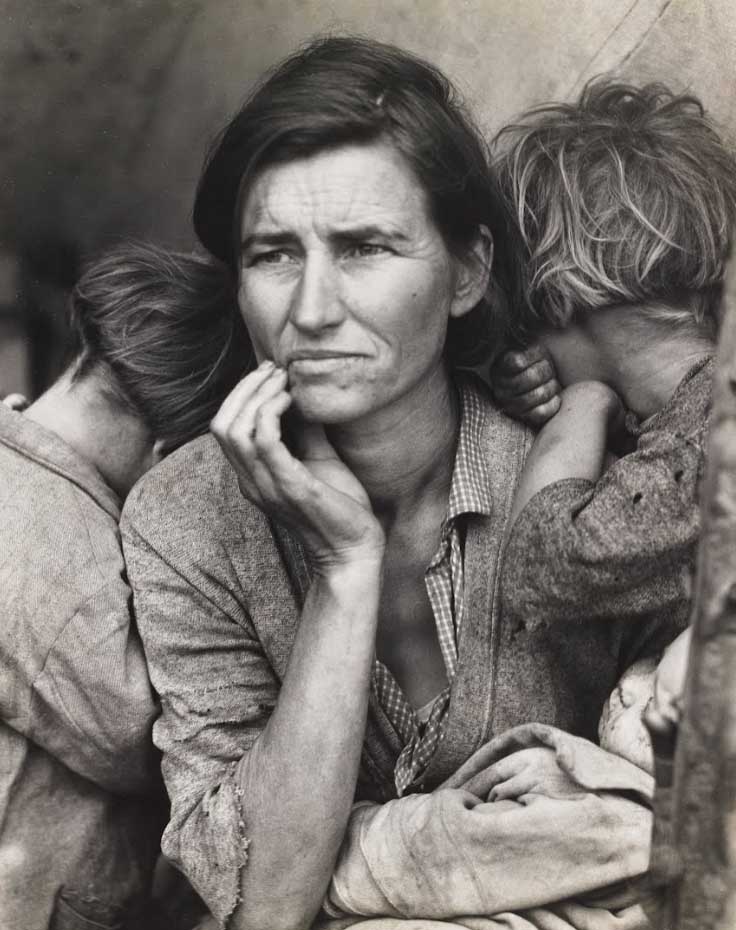

But destitution of the kind which in the thirties stalked the Gorbals, Bowery and slums of every Western city? Which came hand in hand with rickets, polio and TB? Few alive today remember such things. For that we must turn to Steinbeck, Orwell and those harrowed faces captured in the lens of Dorothea Lange.

I wrote the above in a steel city post four years ago, on the Kurds in Syria. But Michael Rosen’s words on fascism – I sometimes fear that people think it comes in fancy dress, with endless re-runs of the Nazis – apply also to poverty. Even in the Empire Metropolis, euphemistically known as “the West”, it is back, though the forms it takes are unlikely to be precisely the same.

In Lidl I note the onwards and upwards surge of prices. A bottle of virgin olive oil which a year ago cost £1.99 is now £3.89. Cold pressed rapeseed oil is £2.89. Last year it was £1.49. Granted, these may not be mainstream family items but it’s the same with eggs, bread, and any number of food and household basics.

Ditto fuel, for reasons including but not confined 2 to the war the US ruling elite is waging not only on Russia, where it has backfired, but also – though this is less advertised – on its biggest trade competitor, the EU. Ditto the cost of money, hence of renting – whether that rent is paid to a landlord or mortgage lender.

For me these things irk but do not inspire dread. I’m comfortable, but aware of the devastating impact on millions of mums who, for all the secondary differences, would surely recognise the haunted face of Lange’s migrant mother, and know something of the gnawing forebodings it speaks to.

On the face of things the reasons are diverse. War in Ukraine … the just-in-time supply chains of the West’s FIRE-led economies … a car crash Brexit. 3 But over and above all these things is the economic illiteracy – if we’re being kind – of both the Conservative Party and a Labour restored, after the blip of the Corbyn years, to its status as a party which Britain’s own ruling elite – and its media – may safely endorse now the A Team is devouring itself.

*

The worldview of tax specialist and modern monetary theorist Richard Murphy is far removed from my own. 4 And since I’ve raised the subject, his evidence-defiant persistence in referring to “Putin’s war” strikes me as a fine example, given Richard’s valuable insights on other aspects of our class divided society, of the Gell-Mann Amnesia Effect.

Be that as it may, within the confines of his ideologically truncated understanding, the man can be witheringly on target. Yesterday’s offering is a case in point. Over to you, prof.

Banks do not lend savers’ money

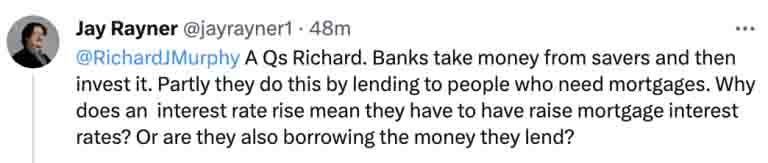

I was asked this question on Twitter this afternoon:

This was my reply (over six tweets):

Thanks for your question Jay. Your question is based on a common misconception that banks lend savers’ money. Actually, they don’t. The Bank of England finally admitted this in 2014. When a bank lends, it creates new money out of thin air. There really is a magic money tree.

That new money then creates deposits in bank accounts. In other words, lending creates savings. But savings are never needed for a bank to make a loan.

All this is because money is nothing more than debt. If I promise to pay the bank £20,000 and they promise to pay £20,000 to the garage I want to buy a car from our mutual promises to pay create that new money. And when the loan is repaid that money is cancelled.

So what do savings do in the macroeconomy? Absolutely nothing at all in most cases. Banks know that. That is why they are so reluctant to pay for them. They are cheap capital for them, maybe, but that’s it. They’re just dead money.

That’s also true of most pension saving by the way – when most is saved in second-hand shares and second-hand buildings and no new value is created by the saving, at all, in mostly cases.

If this was properly understood we could radically change our economy for the better. It isn’t understood because the powers that be (banks and big finance) want us to think they’re really useful. Mostly they’re not, and won’t be until we make them funders of green investment.

* * *

- “I’d be seven or eight …” Since I’m now seventy, I speak of the early ‘sixties, before the advent of supermarkets, with shopping done in the local community and the grocer’s store a hub of gossip.

- Britain’s rulers continue to get away with the devastating effects of a hyperfinancialised economy, and the fire sales decades ago of utilities including energy. But another and more recent reason for high energy prices is no less significant. OPEC defiance of Joe Biden, in refusing to increase production – both to weaken Russia and soften the impact on US voters at the filling station and on their home fuel bills – heralds a seismic shift in the ability of the US Empire to strongarm the world. You wouldn’t know this from ‘our’ media but that shift, or to be precise Washington/Wall Street resistance to it, is what is bringing today’s world so perilously close to Armageddon.

- With peg on nose I voted ‘Remain’ in 2016, though most of my arguments since have been directed at the blinkered smugness of many who voted the same way. For the why of that, try searching this site on the term, Brexit.

- I often quote Professor Murphy approvingly, though always with variations on the caveat attached here. My initial hostility, as a Marxist, to MMT was driven by my own limited understanding. For reasons beyond my scope, money is not a commodity (nor did Marx see it as such) so not subject to the law of value. MMT advocates – not just Richard but leading lights like Stephanie Kelton – often seem to me naive but on this central premise they are correct. In an economy with its own fiat currency, money is indeed created out of thin air. This is not a prescription, a wish or a demand. It is a description of what actually happens.