Michael is the world’s best economist not only in expertise but in moral rectitude, fighting for the liberation of mankind. By “economist,” I invoke the meaning of the term in classical Chinese. The contemporary Chinese term “economy” – jingji – derives from jingshi jimin, used in the 4th to 6th century to mean “governing the world and caring for the people.” This classical sense of the term is most appropriate to describe Michael as an “economist”, as he has been concerned not with the narrow workings of the status quo of market production and consumption, but with how the world is governed, and how people take care of themselves and are taken care of.

See also, Why read Michael Hudson? Part 1. That post concluded with Wen Tiejun, author of the first of two forewords to Michael Hudson’s 2022 book: The Destiny of Civilization: Finance Capitalism, Industrial Capitalism or Socialism.

This post offers the second and – at over 4800 words – longer foreword by Lau Kin Chi. Given its length, and the shortness of this introduction, I’ll drop my usual practice of highlighting third party passages in red. Though undifferentiated by font or colour, the heartfelt and sparkling lucidity that follows – as insightful on the man as on the political economist – is hers alone.

*

How an Economist is Tempered: The Contributions of Michael Hudson to Humanity’s Future

Lau Kin Chi – Director, Executive Team, Global University for Sustainability, Centre for Cultural Research and Development, Lingnan University, Hong Kong, China

A favorite book of my generation was Nicolai Ostrovsky’s 1936 novel, How Steel was Tempered, with its famous quote:

Man’s dearest possession is life. It is given to him but once, and he must live it so as to feel no torturing regrets for wasted years, never know the burning shame of a mean and petty past; so live that, dying, he might say: “all my life, all my strength were given to the finest cause in all the world—the fight for the Liberation of Mankind.”

When I was young, I copied this in my diary to remind myself that every moment should be given to the fight for the liberation of mankind. Many friends of my generation were similarly affected. Starting to write the foreword to Michael Hudson’s book, The Destiny of Civilization, this quote was the first thing that came to my mind. Having come to know Michael as a person and intellectual, working together intensely on his lectures and book projects, I find him to be dedicated with a single mind, not wasting a moment of his life on less relevant matters. I saw from our e-mail correspondence that he often sat writing for 15 hours a day, at the age of 82. This self-discipline stems, I believe, from an adamant will to give all his strength to the finest cause in the world.

Economist on governing the world and caring for the people

Michael is a world-renowned economist. Here’s what has been said about him:

Michael Hudson is surely the most innovative, and in my view, the most important economic historian of the last half century. There are few people alive who have taught me more than Michael Hudson.

David Graeber, author of Debt: The First 5,000 Years, and co-organizer of the Occupy Wall Street Movement

Michael Hudson has consistently been an eloquent, erudite, accurate analyst of the strengths and failings of modern capitalism. He is one of the prescient few who anticipated today’s never-ending economic crisis, and one of a smaller number still whose advice about how to end the crisis would actually work.

Steve Keen, author of Debunking Economics

Michael Hudson is the best economist in the world. Indeed, I could almost say that he is the only economist in the world. Almost all of the rest are neoliberals, who are not economists but shills for financial interests.

Paul Craig Roberts, former Under-Secretary of the U.S. Treasury

The above is no exaggeration. I would add that Michael is the world’s best economist not only in professional expertise but in moral rectitude fighting for the liberation of mankind. By “economist,” I would invoke the meaning of the term “economy” as used in classical Chinese. The contemporary Chinese term “economy” (jingji) is derived from the term jingshi jimin, used in the 4th to 6th century and literally meaning “governing the world and caring for the people.” This classical sense of the term is most appropriate to describe Michael as an “economist”, as he has been concerned not with the narrow workings of the status quo of market production and consumption, but with the way the world is governed, and how people take care of themselves and are taken care of. His erudite concerns are presented in this book, aptly entitled The Destiny of Civilization.

Eminent scholar and erudite writer

Michael is president of the Institute for the Study of Long-term Economic Trends (ISLET), which he founded in the 1990s to coordinate a joint project with Harvard University’s Peabody Museum to create an economic history of the Bronze Age Near East and trace the transformation of economies in their political and social context over the past five thousand years. Like all his work, this has not merely been about understanding the world; his prime motivation has been his endeavor to create a better and fairer world.

One can imagine how a person of integrity, proposing genuine conceptual and practical alternatives to end polarized wealth and power, and, above all, particularly intelligent and competent, would be a threat to corporate and financial interests, their state agents, media propagandists, and mainstream academia. Yet his analysis is so pragmatic and backed by statistics that despite the controversial nature of his critique of mainstream assumptions and theories, Michael remains widely respected for the dozen books he has written.

His op-eds have been published in the Financial Times, New York Times, Washington Post, and major European papers, such as the Frankfurt Allgemeine Zeitung. His numerous cover stories for Harper’s magazine gained him international recognition for not only predicting in 2006 the imminent 2007-08 junk-mortgage crisis, but also for diagramming the financial overhang that was causing the crash and leaving debt deflation in its wake, an analysis that he had earlier presented in articles in books published with his colleagues at the University of Missouri at Kansas City (UMKC) and at the Levy Institute at Bard College.

He is a frequent guest on a broad range of TV and radio programs, including National Public Radio’s Marketplace reports, Democracy Now, and numerous Russia TV shows. He is on the editorial board of Lapham’s Quarterly, is a regular contributor to the e-blogs Naked Capitalism and CounterPunch, and maintains his own website at michael-hudson.com providing access to his frequent public interviews and articles.

Michael has had several books published in Chinese (with more coming soon), and is well known and respected in China. The Chinese Academy of Social Sciences has published numerous articles by him. He has been honorary professor at Huazhong University of Science and Technology in Wuhan, and a professor at the School of Marxist Studies at Peking University. I had read him long before we became acquainted. It was only in May 2016 that we met for the first time, in the company of Samir Amin. Samir and Michael were attending the First World Congress on Marxism held in Beijing.

I introduced to Michael the work of the Global University for Sustainability (Global U), of which Samir and I were among the initiators. Michael gracefully accepted to become one of the Founding Members of the Global U. In May 2018, on the occasion when he, Samir and David Harvey were invited as speakers at the Second World Congress on Marxism in Beijing, I interviewed him on his life and thought – https://our-global-u.org/ oguorg/en/michael-hudson/ – and was struck by his demeanor of gentleness as a person and poignancy as a thinker. In the one-hour interview, Michael told his story which was simply amazing, explaining how his tempering as an economist is a combination of chance and the logic of the circumstances of his time.

Between music and economics— modulation to a higher overtone key

We might have seen Michael as a conductor and music theorist, which was his career aspiration as an undergraduate at the University of Chicago, studying for his BA in Germanic philology and the history of culture. At the same time, independently, he became the master-student of Oswald Jonas, the collaborator of the German music theorist Heinrich Schenker emphasizing counterpoint as driving the structural harmonic progression forward by dissonance resolving itself. To Michael, this unfolding of the overtone system by modulation to a higher key was a musical analogue to the dynamic of social evolution.

Michael’s decision to shift to economics was dramatic. One evening, after moving to New York to publish the works of Schenker, George Lukacs and others, he had dinner with Terence McCarthy, an Irish communist and translator of Karl Marx’s Theories of Surplus Value. The conversation turned to how changes in water levels caused crop failures in the United States that led to an autumnal drain of money from the stock and bond market, and hence to periodic financial crises. In Michael’s words, “to me, these interconnections between production, finance and the overall economy’s systemic relationships were so beautiful, so aesthetic in their unfolding—like musical counterpoint leading to modulation to a higher overtone key—that I decided on the spot to become an economist.”

Ever since, he says, he has been able to achieve in his economic writing what he could not have in music. Michael’s first training followed his acceptance of the condition Terence McCarthy set to mentor him: that he would read all the works in the bibliography of Marx’s Theories of Surplus Value. So while taking his graduate degrees and working for Wall Street banks, Michael also worked part-time for the publisher Augustus Kelley to recommend and write introductions to reprints of economic classics. In the process, he acquired a library of books by economists missing from the “normal” history of economic thought.

Childhood and teenage experience—in an adversarial position

Michael’s disposition certainly has a lot to do with his family and social background during his formative years. He was born in March 1939 in Minneapolis, Minnesota, into a family of labor activists. Of all the cities in the world, Minneapolis had the strongest Trotskyist influence. Michael’s father, Carlos Hudson, had worked with Leon Trotsky in Mexico and been one of the leaders of the great Minneapolis general strike of 1934, as editor of the Northwest Organizer. His father loved Huckleberry Finn, and Michael was called “Huck” by family and friends. But since his father’s party name was Jack Ranger, Michael as a boy also was nicknamed “The son of the Lone Ranger.”

When Michael was three years old, Carlos Hudson was jailed under the Smith Act as one of the Minneapolis 17. Carlos remarked that his year in prison was the happiest time of his life, being assigned to the library, where he collected a long list of proverbs that Michael reproduced on his blog in June 2017. Reading “Dad’s Many Proverbs,” one might come to see not only how J is for Junk Economics came to be structured, but also where Michael’s remarkable sense of humor and witty comments can be traced. When he was growing up in Chicago, visitors to his house included former German colleagues of Rosa Luxemburg and Karl Liebknecht, and members of the Third International when Lenin was still alive and in power. There was almost constant discussion of socialist doctrine and tactics in the meetings convened in his home.

When Michael was 14 years old, in the University of Chicago’s high school, he was called a fascist by Stalinists and a communist by fascists. He told me, “I was very happy being in an adversarial position, yet also the reasonable voice avoiding ideology. I liked being hated by the right-wing because it made me a lot of friends and I recruited many members into the socialist youth groups in Chicago.” Getting more confident and stronger when put in an adversarial position probably has been one of the key traits of his life. Michael has never accepted the world as it is, with its frauds, hypocrisy and injustice. Yet it has taken more than self-confidence and a strong spine to become the great economist that he is today. One reason for his brilliance and uniqueness is that he has not been swayed by his academic training in the unrealistic theories of the economics schools in the universities that justify rather than critically challenge the status quo. Michael has developed his analytic ideas through his real-life work experience in many countries, combined with his deep understanding of the history of economic thought.

Wall Street bank experience—countering ideology.

While employed by Wall Street banks as a statistical economist to understand how the financialized economy works, Michael studied for a Master’s and then a PhD degree in economics at New York University. According to him, most teachers in the master’s program at NYU were part-time. The relatively few full-time academics had no experience working in a bank or corporation; their worldview came from textbooks. Michael fortunately found out for himself how the banks worked, starting as a statistical analyst for the Savings Bank Trust for three years, and then as balance-of-payments economist for the Chase Manhattan Bank from 1964 to 1967. Initially, Michael’s job was to trace how savings were recycled into new mortgage loans by New York’s savings banks. His research showed that most deposits grew not by new saving, but simply by the accrual of dividends at compound interest. This exponential growth was recycled into new mortgage loans to buyers of real estate, seeking ever larger debt/equity ratios in order to dispose of the surplus finance capital. He saw that commercial banks did not lend money to finance new industrial capital investment, but only lent against existing assets, seeking above all to turn their profits or rents into a flow of interest payments.

In short, rents were for paying interest. And increasingly today, so are wages, because payments on bank loans, mortgage loans, student debt and credit-card debt eat away at the disposable income of most families. This is the monthly “nut” that households pay to the Finance, Insurance and Real Estate (FIRE) sector off the top of their paychecks. Later, at Chase Manhattan, Michael compiled statistics to trace how the export earnings of foreign countries were captured into paying debt service. He also traced statistically how U.S. oil companies made profits by “transfer pricing,” selling crude oil production cheaply to tax-free “non-countries” such as Liberia or Panama that used U.S. currency. The oil was then re-sold to refineries in Europe and the USA at a mark-up so high that oil companies had no profits to report, and hence paid no income tax anywhere on their international and domestic operations.

To U.S. policy makers, this exploitation was a success story. In 1966 the oil industry had copies of Michael’s report placed on the desk of every senator and representative, and obtained special favoritism as a result of the sector’s strong contribution to the U.S. balance of payments during the Vietnam War years. The conflict between this reality and academic orthodoxy struck him in 1968 when he had to retake the money-and-banking part of his PhD orals, because his answers were based on his real-world monetary and financial experience, which was at odds with the Chicago School monetarism and vulgarized Keynesian liberalism that had become the academic norm. That was an era when textbooks still taught of helicopters dropping money on the economy—not acknowledging the principle that Michael has made at many monetary conferences ever since: the central bank’s helicopter only flies over Wall Street. Money from this helicopter is lent out to buyers of real estate, stocks and bonds (and to corporate raiders), with little being spent on goods and services.

So the effect is asset-price inflation—which Michael has shown leads to debt deflation as homeowners need to borrow higher and higher mortgage loans to afford the debt-inflated cost of housing, leaving them with less to spend on real goods and services. This now-obvious linkage between rising housing costs and debt deflation was deemed heresy in the 1960s. Mainstream economists thought that as families became wealthier homeowners, they would have more to spend—ignoring the debt dimension of how homes were bought on credit that steadily pushed up the cost of obtaining housing. The Finance, Insurance and Real Estate (FIRE) sector was (and still is) treated as if its rentier income should be added to the economy’s output instead of siphoning it off.

Economic historian—delving into the origins of money and debt

Michael’s experience on Wall Street inspired him to set about investigating the origins of money and replacing the individualistic theories of its origin with a more realistic and historically based explanation. His technical articles and monographs are now accepted as documenting how money originated, not in barter among individuals, but as a means of palatial accounting in Bronze Age Mesopotamia, above all to denominate debts owed to the palace, temples and other creditors in grain and silver as common denominators whose units were set as having equal value for fiscal payments to the palace.

Michael also has shown that instead of interest being invented by individuals lending cattle or grain to reflect productivity rates (as Austrian theory imagines), early interest rates were set by the palaces or other civic authorities simply on the basis of ease of accounting, in terms of the local system of fractions—60ths in Mesopotamia and Egypt, decimals in Egypt and Greece, and the 12-based duodecimal system in Rome (1 troy ounce on the pound per year), increasingly decimalized into 1 percent per month. Finally, he has applied this historical analysis to modern times by showing that throughout history, debts have grown at compound interest faster than the economy is able to pay, leading to foreclosures and economic polarization if the debts are not cancelled. Indeed, for this reason, personal debts were cancelled when new rulers took the throne in Sumer, Babylonia, Egypt and their neighboring lands, in contrast to Greek and Roman oligarchic opposition to debt cancellation and imposition of pro-creditor laws.

Michael’s insights into the workings of modern financialized rent-seeking economies, both within the United States and globally, have prompted him to conduct years of research not only into the origins of money and accounting, but into the origins of labor and how it was paid, the origins of land tenure and taxation, and the origins and history of debt. This analysis has led to his well-known proposition that “debts that can’t be paid, won’t be paid,” and to his advocacy that unpayable debts should be cancelled, and can be cancelled without causing economic disruption—and indeed that without doing so, economies will polarize and crash.

At the World Social Forums, I had marched with tens of thousands of participants, including Samir Amin and Immanuel Wallerstein, with a banner whose slogan “Don’t owe, won’t pay” demanded cancellation of debts for impoverished countries of the Global South. However, I sometimes wondered if the slogan was chanted by many from a political position without a deep understanding of how the debts were generated. The slogan would be meek if it were only a political position to express the distress of the indebted countries and peoples, without an appreciation of why and how the debts should be cancelled. Michael’s advocacy of debt cancellation does not come from a simplistic political position, though certainly the proposition itself is profoundly political. The proposition comes from his insider knowledge of the operation of banks, oil companies, the government and even the military. This experience informed his understanding of the domestic and global politics of the United States, and of the financial dynamics of debt and the long history of debt cancellation in antiquity. Exempt from academic dogmatism and left-wing infantilism, Michael’s economic theories are based on decades of pragmatic statistical and historical inquiry, backed by his earlier training in cultural history as well as his comprehensive reading of Marx’s economic works.

Staunch critic of U.S. Super Imperialism

Working for the accounting firm Arthur Anderson, Michael spent a year analyzing the U.S. balance of payments. His statistics showed that the entire payments deficit resulted from military spending on the Vietnam War and elsewhere. Seeking ways to finance that military deficit led the U.S. Government to ameliorate the worsening balance-of-payments deficit by asking U.S. banks to set up branches in offshore banking centers to attract the world’s criminal capital, from drug dealings to kleptocratic embezzlement (the world’s new “neoliberal” sectors). This outgrowth of oil-industry “flags of convenience” has led to today’s crisis of tax enclaves enabling the world’s wealthy individuals and corporations to avoid taxation and file fictitious economic statistics.

Michael has exposed this in numerous introductions to books and in interviews in documentary films. Michael’s understanding of how the global economy under U.S. hegemony worked enabled him to forecast in Ramparts in 1968 that the USA would have to go off gold, which it indeed did in August 1971. Explaining how ending the gold standard had inaugurated the U.S. Treasury-bill standard that obliged foreign governments to finance the U.S. balance-of-payments and domestic budget deficits, his first book, Super Imperialism: The Economic Strategy of American Empire (1972), gained him international recognition and has been translated into many languages. He had hoped to help countries resist the system of dollarization that has enabled the United States to obtain a free ride for its foreign military spending and takeover of other economies. But from the very beginning, the U.S. Government used the book as a how-to-do-it manual. Michael was quickly employed by Herman Kahn’s Hudson Institute to explain to the White House and the Department of Defense how the new international financial order worked. The success of Michael’s books led many Wall Street and Canadian financial institutions to retain him as a consultant forecasting interest rates and currency exchange rates.

The Canadian government invited him as financial advisor to develop the balance-of-payments dimension of what has become Modern Monetary Theory (MMT), showing that Canada did not need foreign loans to finance its provincial and other domestic spending. His book describing why Canada did not need foreign borrowing for its provinces and companies to spend domestically, Canada in the New Monetary Order (1978), showed that when Canada borrowed abroad, the central bank still had to create domestic money in any case to be spent locally as a counterpart to the foreign currency inflow.

Hardly by surprise, this led to passionate attacks by Canada’s banks seeking to profiteer by indebting the economy through their loan underwriting. But it also led to further contracts with Canada’s State Department and Science Council. In the late 1970s, Michael was invited by the United Nations Institute for Training and Research (UNITAR) to become economic advisor on North-South debt and trade. He warned of the coming Latin American debt defaults, which indeed began in 1982 with Mexico. He subsequently has served as economic advisor to numerous governments, agencies and political parties from Latvia to Greece. He has argued for national protectionism and capital controls to resist free-trade imperialism, for domestic money creation to finance domestic spending on less inflationary terms than borrowing foreign currency, and for the need to tax and limit rentier gains in real estate and finance.

Academic and theoretical contributions

Michael has worked within academia on sustained intellectual inquiry. For many years he was on the economics faculty of the University of Missouri at Kansas City (UMKC), which became the center of MMT in the early 2000s with Randall Wray, Stephanie Kelton and Bill Black. He was Economic Research Director at the Riga Graduate School of Law (RGSL), where he became Chief of the Committee of Experts for the Renewal Task Force Latvia (rtfl.lv). As for his most well-known academic inquiry, that into the history of debt and money, he was appointed a research fellow in Babylonian economics at the Peabody Museum of Archeology and Ethnology at Harvard University, where he organized a colloquium every few years from 1994 onward. The five volumes of conference colloquia that he has co-edited have rewritten the economic history of the ancient Near East and classical antiquity. These colloquia were on privatization, land tenure and real estate ownership (which were found to be based on fiscal liability), debt cancellation and economic renewal, the origins of money and accounting, and the origins of labor services (discovered to have arisen to work on public infrastructure and to work off personal debts).

The findings of these colloquia and their members refute previous libertarian individualistic theorizing on economic origins, and have now become the new orthodoxy among Assyriologists, Egyptologists and anthropologists, most notably Michael’s friend David Graeber, who wrote his book Debt: The First Five Thousand Years, largely to popularize Michael’s approach. The essential focus of the colloquium volumes is on how money, interest-bearing debt and land tenure were innovated in the palaces and temples of the ancient Near East, and on how the privatization of money and credit led to the polarization in ownership of land and other wealth in the hands of private oligarchies from classical antiquity to today’s Western economies.

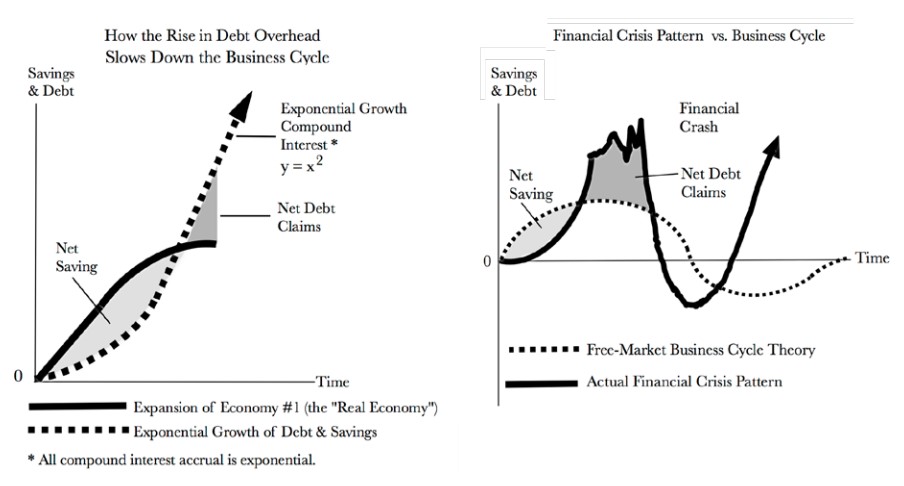

As one of the few economists who predicted the 2008 crash, Michael published one of his most important theoretical papers in 2006: Saving, Asset-Price Inflation, and Debt-Induced Deflation. It accurately explained how the exponential expansion of credit created corresponding debt that would lead to the impending financial crash and its aftermath. On September 8, 2009, Dirk Bezemer wrote an article in the Financial Times – Why some economists could see it coming – which stated:

Michael Hudson of the University of Missouri wrote in 2006 that ‘debt deflation will shrink the ‘real’ economy, drive down real wages, and push our debt-ridden economy into Japan-style stagnation or worse.’ Importantly, these and other analysts not only foresaw and timed the end of the credit boom, but also perceived this would inevitably produce recession in the US.

That article included the set of charts that helped make Michael famous for his explanation of why financial crises are endemic and lead to secular stagnation: Today, with the world in deep financial crisis, Michael has reiterated his proposition that unpayable or odious debts should be cancelled, and indeed must be cancelled in order to avoid a global austerity crisis and economic polarization stemming from chronic debt deflation.

One point of clarification here. The United States has become the world’s biggest debtor, mainly as a byproduct of the fact that most international debts are denominated in dollars. This poses a basic question: Which debts should be wiped out? Michael urges that the debts of overindebted households and impoverished countries in the Global South should be written down, but that one debt should not be cancelled: the official foreign debt of the U.S. Government. The United States has run up this official foreign debt—like its domestic Treasury debt—without expecting ever to actually pay it off. It has no intention of imposing on itself the austerity that it and the IMF demand of other debtor countries. This asymmetry, along with the U.S. sponsorship of today’s New Cold War, has led leading dollar-holding nations such as China and Russia to begin de-dollarizing their economies. This signals the fracturing of the world economy that Michael predicted in his 1977 Global Fracture. The United States is forcing other countries to choose between accepting a dollarized and militarized rentier austerity, or going their own way by creating mixed public/private growth-oriented economies.

For socialism

For us on the Global U team, it has been a great privilege and honor to be learning from Michael, face to face. He was invited to give lectures in Hong Kong and Macau in November 2019, during which he had a dialogue with Wen Tiejun on economic and financial issues in China. During the Seventh and Eighth South-South Forums on Sustainability in 2020 and 2021, he had further discussions with Wen Tiejun. Michael has a particular concern for China’s development, as he feels that China is the leading exception to the U.S.-based neoliberal economic model, not taking the destructive advice of the IMF and World Bank. He has argued that China’s economy can be resilient if it organizes its real estate, debt and tax system to avoid the rentier financialization process that is destroying the West.

In September 2020, while we were chatting online, I sounded the idea that Michael give a lecture series for Global U. Michael accepted on the spot. I emailed him a proposal of 10 topics, and within five hours he came back with a detailed outline. The lectures were delivered weekly in September-December 2020. Rewriting these lectures to create the current book took another few months. I sometimes wonder whether Michael would have had second thoughts if he had known that his spontaneous acceptance of my request would take ten months of his time. But fortunately for readers, this became a blessed opportunity to access his central ideas and be guided to his dozen books. The videoed lectures, subtitled in Chinese and divided into 70 episodes, were screened in April-August 2021 in China.

The first episode has been watched by over 188,000 viewers, with 30,000 viewers on average for the remaining episodes. The English-subtitled lectures are available on www. michael-hudson.com. What readers now hold in their hand, the book written on the basis of these lectures, presents Michael’s dissection of the burning global issues of today, and his explanation of how the industrial capitalism analyzed in the 19th century by Marx and other classical economists has turned into finance capitalism based on debt and rent extraction. This financialized system is polarizing the Western economies and threatening their collapse in a wave of foreclosures and new privatizations by a financial oligarchy. Most important are Michael’s proposed alternatives for de-dollarization and de-privatization to avoid global debt deflation and New Cold War imperialism. Indeed, if civilization is to avoid the destiny of destruction, if humanity is to have a future, socialism is the only way—and that is what Michael has passionately argued in this book.

* * *

Thank you for this Philip. It is a valuable service.

My pleasure, bevin